The usual method is to create an identical trust for each beneficiary. If you do not want to create similar individual trusts for each child or need a trust for a specific purpose, there are other trusts to choose from, depending on the person and the situation.

- The trust should include specific details that direct how and when the assets may be available to beneficiaries. For example, you can designate that assets must be:

- Dispersed or sprinkled over a certain time, at a certain age, in specific amounts, or at certain intervals; or

- Used for educational expenses or a downpayment on a house.

- Each beneficiary is a beneficial owner and is entitled to a certain proportion of the trust income, depending on the terms of the trust. This may include receiving a monthly allowance, receiving the money at a certain age, or claiming funds at any time.

- The trust will usually set an expiration date when the beneficiary receives the balance left in the trust. This usually depends on the beneficiary and the situation.

- Trusts for minor children cannot expire until they reach the age of maturity, typically 18 years old.

- A special needs trust for a disabled beneficiary may have no expiration date as long as the trust is funded or only expires when other resources like Medicaid, Medicare, Social Security, or Welfare become available.

- Other expiration dates are discretionary but may include: the beneficiary turns 25 years old, graduates from college, or gets married. You may want to leave it up to the discretion of the trustee as to when the beneficiary is ready, but 35 years old is the limit.

- If created in your will, the executor is theoretically responsible for naming the trustee but you can designate one if you want a different person.

- Some of these trusts, such as the discretionary trust and stand-alone third-party special needs trust, can be created for use while you are alive.

It is possible to create a testamentary trust in either your will or a living trust (rarely). This is done by including the testamentary trust details in your will or a clause in a living trust. You can alter the terms of the testamentary trust while you are alive by updating your living trust, will, or the appropriate codicil.

It is possible to create a testamentary trust in either your will or a living trust (rarely). This is done by including the testamentary trust details in your will or a clause in a living trust. You can alter the terms of the testamentary trust while you are alive by updating your living trust, will, or the appropriate codicil.

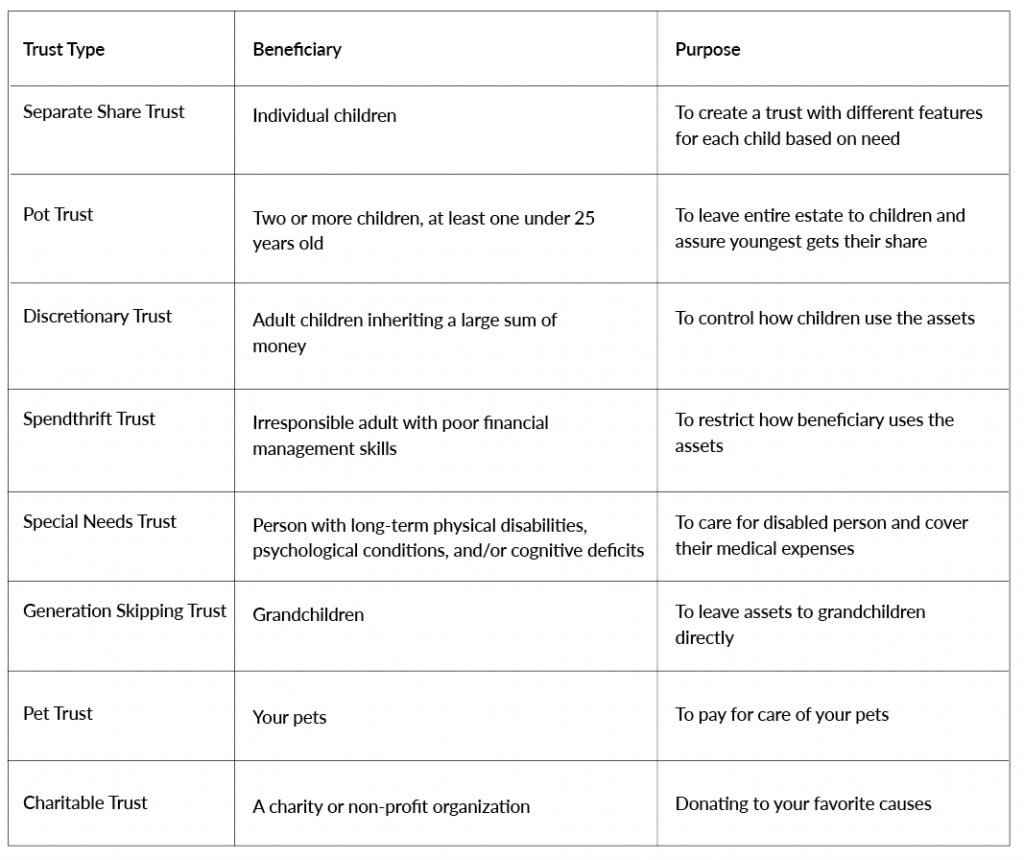

A Separate Share Trust is similar to the standard testamentary trust, but with each child’s trust having different assets and features specific to their situation and needs.

A Separate Share Trust is similar to the standard testamentary trust, but with each child’s trust having different assets and features specific to their situation and needs.

Because receiving different amounts of your assets can create resentment among siblings, especially if created in your will when each child can learn what the other is inheriting, it may be best to discuss it with them beforehand. It is a form of Sprinkling Trust.

You can consider a standard testamentary trust created for minors to be a discretionary trust since minors cannot manage financial interests. In this case, you need the trustee or conservator to use your instructions and their discretion to manage the trust for them and use it to provide for their needs.

A discretionary trust is created using a discretionary deed of trust and usually chosen for a spouse or adult children inheriting a large sum of money.

- Although discretionary trusts can be created and used while you are still alive, they are most commonly used for assets that go to beneficiaries upon your death

- These include assets in your will, a living trust, or payable on death accounts, like bank accounts, certificates of deposit (CDs), money markets, or a life insurance settlement, that name the trust as beneficiary.

- In addition to stipulating when the trust expires and when/how the beneficiary receives the remaining assets, you can specify:

- How much money the beneficiary can get at one time and the intervals between the gifts;

- What the money can be used for, such as education, medical bills, every day expenses, etc.; and

- The age they can start to receive money.

- Unlike the standard testamentary trust, there is no age limit on when the funds assets have to be transferred to the beneficiary, so the trust can be a lifetime trust.

This is typically done to protect assets from a beneficiary’s poor money-management skills, extravagant spending habits, gambling or drug habit, personal or professional creditors, lawsuits, divorced spouses, predator’s/scams, etc.

- With guidance from details in the trust, the trustee has full discretion of the distribution of money and assets to the beneficiaries. However, they are not obligated to follow your guidance.

- As long as the trust exists, the funds are not part of your beneficiaries’ estates. They have no individual access to the funds and cannot claim or demand money from it.

- Like many trusts, a discretionary trust can be designed to minimize estate taxes since the trust assets pass directly to the beneficiaries.

- You can designate future beneficiaries for any assets remaining after your beneficiaries death, such as a grandchild.

A trustee is chosen who can name beneficiaries if they are otherwise unspecified and has complete control to manage the finances until a pre-specified time, until the beneficiaries are capable of managing them as determined by the trustee, or the lifetime of the beneficiary.

A trustee is chosen who can name beneficiaries if they are otherwise unspecified and has complete control to manage the finances until a pre-specified time, until the beneficiaries are capable of managing them as determined by the trustee, or the lifetime of the beneficiary.

- The trust/trustee is protecting your estate by protecting the beneficiary from themselves.

- You will be able to add provisions to protect assets from creditors and to provide any guidance, such as a letter of intent, to the trustee you deem necessary, consistent with established bankruptcy and creditor protection laws.

- You may want to arrange for oversight of the trustee. This may done by:

- Having one or more “appointer” with the power to remove the trustee and appoint a new one; or

- Appoint a guardian who has the power to veto your trustee’s decisions.

Although very much a part of our lives, we often forget about including our pets in our Estate Plan. While animals may not be able to inherit money or property, you can assure they can be cared for after you die or if you can no longer care for them. These pets may include: cats, dogs, birds, turtles, snakes, lizards, hamsters, and similar small animals. You could also set up a pet trust for larger animals, such as a horse.

Although very much a part of our lives, we often forget about including our pets in our Estate Plan. While animals may not be able to inherit money or property, you can assure they can be cared for after you die or if you can no longer care for them. These pets may include: cats, dogs, birds, turtles, snakes, lizards, hamsters, and similar small animals. You could also set up a pet trust for larger animals, such as a horse.

While you can leave your pet to a beneficiary in your will and include funds to care for them, you may have little control of how they take care of your pet or spend the money. A pet trust can allow you to do both.

The 1990 Uniform Probate Code stated that a trust for the care of your pets can be created in all states, although there is some state-to-state variation. For most states the terms of the trust is for the rest of a given pet’s life. Some limit the duration of the trust to 21 years after your death, others up to 90 years. The trust cannot include provisions to care for other pets your caretaker may acquire.

Like other types of trusts, a pet trust will appoint a trustee. You will also appoint a caretaker, that may be different from the trustee, who will have custody of your pet and be responsible for their day-to-day care. You can also appoint a separate trust protector or enforcer to make sure your wishes are carried out.

Like other personal representatives, it is best to discuss it with them and to choose an alternative.

Consider the number of pets you have, their age, health, standard of living, grooming needs, and other needs when estimating how much to put in the trust. If the amount seems excessive, your family can contest the amount.

There are many other considerations to think about when deciding on the terms of the trust.

- To avoid fraud, make sure you have an accurate way to identify your pet, such as a detailed description or embedded chip.

- You may want to provide very detailed instructions for the caregiver, such as favorite food and toys, ‘puppy play dates,’ walking habits, grooming, and sleeping arrangements.

- Include any medical information, including your preferred veterinarian.

- You can include instructions that the trust takes effect if you are no longer able to care for your pet.

- Who will be the beneficiary of any remaining money in the trust.

- What burial or cremation arrangements that you would prefer once your pet passes away.

Preparing to create a testamentary trust is similar to a living trust and involves finding all your assets and making decisions about the type of trust, trustee, and specific details of its contents.

Preparing to create a testamentary trust is similar to a living trust and involves finding all your assets and making decisions about the type of trust, trustee, and specific details of its contents.

- Make a list of all the assets you have.

- Include tangible items such as your house, car, and jewelry, and intangible items such as stocks, bonds, and patents.

- Include financial assets such as life insurance policies, retirement accounts, annuities, bank accounts, certificates of deposit (CDs), money markets, and any other financial assets you want to include by making the trust the beneficiary.

- Omit any financial assets or property that is jointly owned or you would prefer to be transferred using a transfer on death deed or payable on death account. Even if they were included, the beneficiary designation in the trust will be overridden by the beneficiary designation in the other document.

- Choose the type of trust that is appropriate for your situation, such as those described above.

- Choose the beneficiaries.

- This is usually family and friends but may include organizations (including charities) that will receive assets upon your death, as well as who will get what.

- You may want to decide on those who you don’t want to include and the reasons why.

- Decide on the specific assets, including amounts, that will go to each beneficiary.

- The decision will be known to all beneficiaries if the trust is created in your will.

- Even if created in a trust, where the decision is only available to the inheriting beneficiary, it is still better to discuss the distribution with all beneficiaries if it is to be unequal.

- Choose a trustee that will manage the estate.

- The trustee chosen should be a person, usually known to you or the executor, with integrity that can be trusted implicitly.

- The other qualities you would like to have in a trustee are the same as those laid out in Choosing an Executor and Trustees – Who to Choose.

- They should be aware of their duties before they agree to serve as trustee.

- Other qualities may be needed for some types of trusts, such as a Special Needs Trust or Spendthrift Trust.

- Consider and include instructions about how you would like the trustee to manage the trust and distribute individual assets.

You can either transfer assets directly to adult beneficiaries or leave instructions on how the assets are to be distributed and/or how they may be used.

You can either transfer assets directly to adult beneficiaries or leave instructions on how the assets are to be distributed and/or how they may be used.- Minor children cannot own assets; your trustee will need to control and manage the assets until they are at least 18 years old or reach another milestone, such as finishing college.

- While you can include any level of detail to guide the trustee in handling financial matters and adapting to changes, you won’t be able to anticipate everything. You need to consider the possibility that things can change and issues may arise that require different actions of the trustee other than those specified in the trust. These may include:

- Shifting needs of the beneficiaries over time;

- Changing dispersion of the trust if a beneficiary dies;

- Changes in what the beneficiaries have to spent their money on, such as medical bills instead of educational costs;

- Investments to be made with the trust; and/or

- When the trust expires.

- There are two ways a trustee can adapt to these changes and deal with unexpected issues:

- They can ignore your instructions, as there is no legal obligation for them to do so; or

- You can officially give them the power to ignore them.

- Choose a guardian for your minor children.

- You cannot designate a guardian through a trust. You need to consider who you would want to take care of them in case both you and your spouse die.

- A guardian can be designated in a pour-over will, which should be created at the same time as your living trust. This will provide for the distribution of any new assets not added to your living trust before your death or any assets inadvertently excluded.